UI Return on Equity Slips Again, Falling to 3.49 Percent in First Quarter 2025

Company’s profitability falls to its lowest level ever, continuing a trend of financial degradation seen since PURA’s most recent rate case decision in 2023

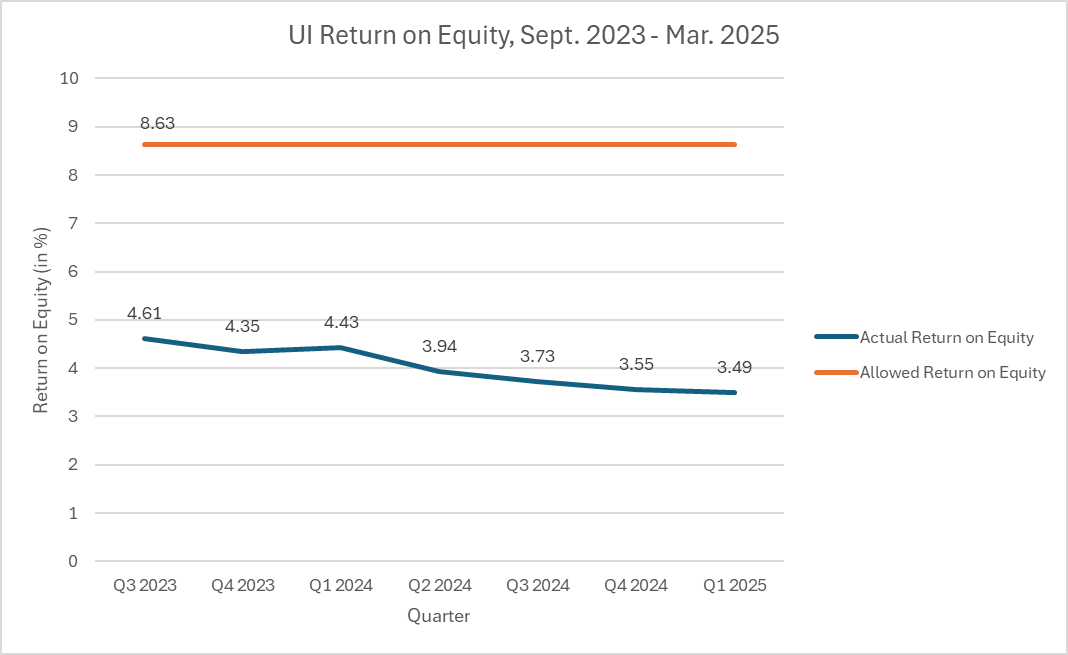

A graph demonstrating UI’s Allowed Return on Equity vs. its Actual Return on Equity, from Sept. 2023 through March 2025

ORANGE, Conn. — May 12, 2025 — Today, Frank Reynolds, President and CEO of United Illuminating (UI), a subsidiary of Avangrid, Inc., issued the following statement regarding the company’s Friday filing with the Public Utilities Regulatory Authority (PURA) containing its first-quarter Return on Equity of 3.49 percent:

“Nothing good comes from a utility that is financially devastated. PURA commissioners recognize that. Legislators recognize that. Even our fiercest critics and opponents recognize that, at least in theory, energy companies like UI provide an essential service to our customers, and accordingly, regulators must enable them to do so.

“Yet in practice, too many of these stakeholders are willing to overlook or dismiss the harms we have continued to raise about the financial state of our company. Perhaps it’s easier to fall back into easy tropes about businesses like ours ‘taking advantage’ of our customers. Or perhaps it’s politically inconvenient to question the consequences of PURA’s current leadership, whose inconsistent application of regulatory law and procedure has led directly to today’s dismal returns for UI, one of Connecticut’s oldest companies.

“Whatever their reasons, it is becoming harder and harder for any of these stakeholders to ignore the facts: because of PURA’s decision in our rate case in 2023, our revenues have been entirely deficient to provide our essential service – the distribution of electricity – to a growing customer base.

“The impacts will harm our customers in every way. A Return on Equity of 3.49 percent makes debt investors nervous, and the premiums they will require to buy UI’s debt will end up on customers’ bills in the form of higher rates. That will force UI to limit its investments to only the most basic and necessary to keep the lights on in the immediate term. Longer-term but deeply needed capital investments – such as rebuilding Old Town Substation, a 60-year-old substation serving nearly 18,000 customers in southern Trumbull and Environmental Justice communities in Bridgeport – will have to be deferred.

“It’s not too late to turn this increasingly dire situation around. In our new investment plan filing, which we submitted to PURA in November of last year, we’ve done our part to show what we need to provide best-in-class electricity service. Now, we’re asking our regulators to step in and correct the harms they’ve allowed to continue for far too long, and to provide us the revenues we need for the quality of service our customers expect and deserve.

“Again, no one wins when an energy company faces financial deterioration – certainly not the 345,000 residents and businesses who rely on us to serve them with safe and reliable electricity, 24 hours a day, 7 days a week. It’s PURA’s turn now, and the stakes are high: we hope they’re ready to meet them.” – Frank Reynolds, UI President and CEO

Background:

Return on Equity is a measure of a company’s financial performance, calculated by dividing distribution net income by shareholder’s equity (which is the company’s assets minus its debt). Put simply, Return on Equity measures the company’s profitability.

For an ROE to be sufficient, it must, at the very least, exceed UI’s costs of borrowing, which is currently 4.72 percent. The year-end actual ROE of 3.49 percent is, therefore, substantially insufficient to attract investment, which is essential to funding capital projects and operations. The ROE is also insufficient to allow access to equity, as the cost of equity in the market is not paid.

For regulated utilities such as UI, PURA sets an upper limit on what utilities are allowed to, but are in no way guaranteed, to earn in their ROE. Following PURA’s Final Decision in UI’s 2023 rate case (Docket #22-08-08), the company is authorized to earn up to an ROE of 8.63 percent, inclusive of penalties. However, UI, and any other regulated utilities, are in no way guaranteed to earn their allowed Return on Equity. As the graph above demonstrates, UI is earning less than half its allowed ROE.

A utility company that is not able to attract investment in the market has only two options: either the company must offer investors a premium to incentivize their investment, which are paid for by customers; or the company must defer all capital investments, which are essential to the reliability and resiliency of the energy system.

As a result, UI is deferring investments, like new substations and protective flood walls, to preserve its limited capital for new customer connections, state projects, and only the projects most essential to immediate-term reliability. Without significant improvements, customers will bear the consequences with poorer quality of service and higher rates. These consequences will be worsened as the company’s falling ROE is coupled with decreased credit ratings, as UI’s sister companies (Connecticut Natural Gas [CNG] and Southern Connecticut Gas [SCG]), as well as Eversource and all its subsidiaries, received in December. (See: CNG, SCG Respond to S&P Global Credit Rating Downgrades - SCG and CNG, SCG Credit Ratings Downgraded by Moody’s Ratings; Outlooks Negative - CNG.)

UI filed a new rate case in November 2024 (Docket #24-10-04), asking PURA to increase distribution revenues by $105 million to support more than 200 reliability and resiliency investments across the company’s service area.

SCG and CNG also filed their year-end actual ROEs with PURA on Friday. CNG’s actual ROE for the first quarter of 2025 is 7.48 percent, down from 8.77 percent for the previous quarter and under its allowed ROE of 9.15 percent. SCG’s actual ROE is 6.91 percent, slightly above its previous ROE of 5.84 percent but also well under its allowed ROE of 9.15 percent.

Media Contact:

Sarah Wall Fliotsos

(757) 407-4255